Access information in your language

If English is not your first language, interpreter services are available to help you.

Changes to requirements for New Zealand citizens apply for settlements from 26 November 2025.

Exemptions, concessions and rules for foreign purchaser additional duty

Situations where additional duty does and doesn’t apply.

Key information

Foreign purchaser additional duty applies to foreign purchasers of residential property.

Foreign purchasers include foreign natural persons, foreign corporations and foreign trusts.

Exemptions and concessions from land transfer duty

If a transfer is exempt from land transfer duty, it is also exempt from additional duty. If a transfer only qualifies for a concession, additional duty may still apply.

Spouse/partner

If you are a foreign purchaser acquiring a principal place of residence (PPR) with your spouse/partner, you may be exempt from additional duty if:

- your spouse/partner is not a foreign purchaser

- you live in the property as your PPR for 12 months, starting within 12 months of settlement.

If the transfer is entitled to a first home buyer exemption, then the residence requirement:

- is not fixed on the foreigner

- can be met by any of the transferees.

Whereas for the foreign purchaser additional duty exemption, it is the foreigner who must meet the residence requirement.

Relationship breakdowns

If you transfer property due to a relationship breakdown with your spouse/partner, it may be exempt from land transfer duty and additional duty. Check the criteria.

Property transferred pursuant to a will

If property is transferred pursuant to a will and exempt from land transfer duty, the foreign purchaser does not have to pay additional duty.

Pensioners

Eligible pensioners can still claim a duty exemption or concession when they buy a property with a foreign purchaser. The criteria depend on whether the contract was signed before 1 July 2023 or on or after 1 July 2023.

If the property is exempt from duty, the foreign purchaser doesn’t have to pay any additional duty.

But if the pensioner fails to meet the residence requirement for the exemption:

- they will be reassessed for duty

- the foreign purchaser will have to pay additional duty on their share of the property.

If the property only qualifies for a concession, additional duty may apply to the foreign purchaser’s share.

Principal place of residence concession

A foreign purchaser may qualify for the PPR concession if they meet all the criteria.

However, the concession does not apply to the calculation of additional duty. Additional duty is calculated on the dutiable value of the foreign purchaser’s interest in the property before applying any concessions.

Find out about calculating foreign purchaser additional duty.

Corporate reconstruction/consolidation concession

The corporate reconstruction concession and corporate consolidation concession apply to eligible transactions from 1 July 2019.

The concessions apply on the duty otherwise payable, including any additional duty. Accordingly, these concessions can reduce the foreign purchaser additional duty payable.

New Zealand citizens

Additional duty does not apply to New Zealand citizens who ordinarily reside in Australia for 6 consecutive months within the 12-month period before or after settlement.

‘Ordinarily reside’ means where you regularly or customarily live. It does not include a temporary or occasional residence.

If you are relying on the period after settlement, or a period that spans the settlement date and you know you won’t meet this residence requirement, you must notify us within 30 days. We can use our discretion to adjust this residency period if you have a good reason. Generally, you must not have known the circumstances at the time of the transfer, and they must be outside your control.

Before 26 November 2025

The residence requirement for New Zealand citizens applies to all settlements from 26 November 2025.

Before 26 November 2025, a New Zealand citizen must have held a special category visa (subclass 444) at settlement for additional duty not to apply.

Landholder acquisitions

When a foreign purchaser makes a relevant acquisition in a landholder, land transfer duty applies to the unencumbered value of the landholder’s total landholdings.

If the landholdings include residential property, foreign purchaser additional duty applies by reference to those residential properties. So, when a foreign purchaser makes a relevant acquisition in a landholder, additional duty only applies to the residential share of the total landholdings of the landholder.

Find out about calculating additional duty on relevant acquisitions in a landholder.

Unpaid duty

If we have assessed a transfer that is chargeable with foreign purchaser additional duty because the duty was not paid by the due date, the unpaid duty (and any penalty tax and interest) is a first charge on the land.

The charge – whether registered on title or not – takes priority over all other liabilities concerning the land.

If the charge is not registered and the property is sold, we will not enforce the charge against the new owner.

Foreign corporations and trusts

Exemption for boosting housing stock

An exemption from additional duty is available for foreign purchasers who meet certain criteria. Generally, they must be Australian based and their commercial activities must significantly add to the supply of housing stock in Victoria through new developments or redevelopment.

The exemption can only apply to ignore:

- a foreign controlling interest in a corporation incorporated in Australia, or

- a foreign substantial interest in a trust.

Before applying, refer to the Treasurer’s guidelines issued on 1 October 2018. The guidelines include an example of how build-to-rent developments may qualify for the exemption.

Controlling interest in a corporation

Foreign purchasers include foreign corporations.

A foreign corporation is a corporation incorporated:

- outside Australia, or

- in Australia if a foreign natural person, another foreign corporation or a trustee of a foreign trust has a controlling interest in it.

A person has a controlling interest in a corporation when they (either alone, or together with an associated person or another foreign natural person, corporation or trustee of a foreign trust):

- are in a position to control more than 50% of the votes at a general meeting

- have an interest in more than 50% of the issued shares in that corporation

- the Commissioner determines they can influence decisions about the corporation’s financial and operating policies, considering:

- the practical influence they exert

- any rights they can enforce

- any practice or behaviour affecting the corporation’s financial or operating policies, even if it breaches an agreement or trust.

An associated person can be:

- a relative of the foreign purchaser

- a partner in a partnership

- another corporation with the same majority shareholder as the foreign corporation

- a trustee of a trust in which the foreign purchaser is a beneficiary.

An associated person does not have to be a foreign natural person, corporation or trustee of a foreign trust.

Voting power and potential voting power

The voting power in a corporation refers to the maximum number of votes that might be cast at a general meeting of the corporation.

Potential voting power in a corporation refers to the voting power based on the assumption that the votes might be cast at a general meeting of the corporation including each vote that:

- might exist in the future because of the exercise of a right (whether actual, prospective or contingent), and

- if it came into existence, might be cast at a general meeting of the corporation.

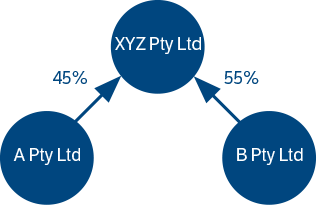

Example

XYZ Pty Ltd purchases land in Victoria. XYZ Pty Ltd is a corporation incorporated in Australia. Its shareholders are A Pty Ltd (45%) and B Pty Ltd (55%).

B Pty Ltd has 2 shareholders. Both are foreign natural persons.

This means B Pty Ltd is a foreign corporation with a controlling interest in XYZ Pty Ltd, which makes XYZ Pty Ltd a foreign corporation.

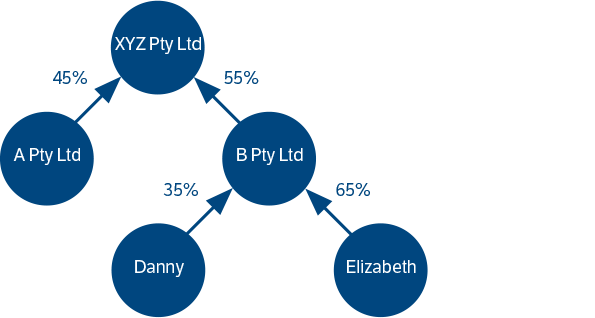

Example

XYZ Pty Ltd purchases residential property in Victoria. XYZ Pty Ltd is a corporation incorporated in Australia.

XYZ Pty Ltd has 2 shareholders: A Pty Ltd (45%) and B Pty Ltd (55%). B Pty Ltd has 2 shareholders, Danny and Elizabeth.

Danny holds an Australian permanent visa and has 35% of the shares in B Pty Ltd. Elizabeth is a foreign natural person who has 65% of the shares in B Pty Ltd.

Elizabeth has an interest in more than 50% of the issued shares in B Pty Ltd and therefore has a controlling interest in B Pty Ltd. This means B Pty Ltd is a foreign corporation.

B Pty Ltd holds more than 50% of the issued shares in XYZ Pty Ltd, so it has a controlling interest. This makes XYZ Pty Ltd a foreign corporation.

Substantial interests in a trust

Foreign purchasers include foreign trusts.

A foreign trust is a trust where a:

- foreign natural person

- foreign corporation, or

- trustee of another foreign trust

has a substantial interest in the trust estate.

A person has a substantial interest in a trust when they (either alone, or together with an associated person or another foreign natural person, corporation or trustee of a foreign trust):

- have a beneficial interest of more than 50% of the capital of the trust’s estate, or

- the Commissioner determines they can influence decisions about the trust’s administration and conduct, considering:

- the practical influence they exert

- any rights they can enforce

- any practice or behaviour affecting the trust’s administration and conduct, even if it breaches an agreement or trust.

A discretionary trust that has any potential foreign beneficiaries is generally considered a foreign trust. Most family trusts are discretionary.

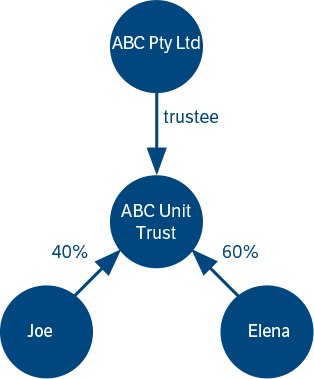

Example

ABC Pty Ltd acts as trustee for the ABC Unit Trust. ABC Unit Trust has 2 unitholders, Joe and Elena.

Joe is an Australian citizen who holds 40% of the units. Elena is a foreign natural person who holds 60% of the units.

Elena has a substantial interest in the ABC Unit Trust, which makes it a foreign trust.

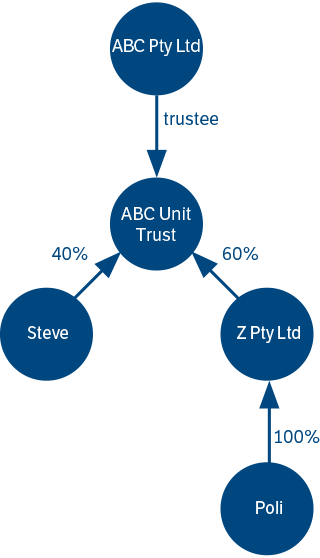

Example

ABC Pty Ltd, as trustee of the ABC Unit Trust, buys residential property. The ABC Unit Trust has 2 unitholders, Steve and Z Pty Ltd.

Steve holds an Australian permanent visa and 40% of the units. Z Pty Ltd is a corporation incorporated in Australia, which holds 60% of the units.

The sole shareholder of Z Pty Ltd is Poli, a foreign natural person. As Poli has an interest in more than 50% of the issued shares in Z Pty Ltd, she has a controlling interest in Z Pty Ltd. This makes Z Pty Ltd a foreign corporation.

Z Pty Ltd holds an interest in more than 50% of the capital of the trust estate of the ABC Unit Trust. Therefore, Z Pty Ltd has a substantial interest in the unit trust. This makes the ABC Unit Trust a foreign trust.