Grouping and land tax

Related corporations may be grouped for land tax purposes.

Key information

Under the Land Tax Act 2005, corporations are related corporations in certain circumstances. Where 2 or more corporations are related, they may be treated as a land tax group.

If corporations are grouped, the land holdings of each corporation in the group are combined and assessed as if they were a single land holding owned by a single corporation (i.e. land tax is calculated on the total taxable value of all land owned by members of a group as if it were a single piece of land held by a single company).

Members of a land tax group are jointly and individually liable for the land tax payable by the group. As such, we are able to recover the land tax payable by the land tax group from any member of that group.

An absentee owner can be a member of a land tax group. Absentee owner rates are available on our website.

Additional guidance is provided in Revenue Ruling LTA-008 - Grouping of related corporations.

Corporations grouped for land tax

Two or more corporations can be related for land tax purposes in various ways. These are where:

- One corporation:

- Controls the composition of the board of directors of another corporation.

- Is able to cast, or to control the casting of, more than 50% of the maximum number of votes that might be cast at a general meeting of another corporation.

- Holds greater than 50% of the issued share capital of another corporation.

- A person has, or persons together have, a controlling interest in each of those corporations. There are 3 ways in which a person or a set of persons may have a controlling interest in a corporation. These are:

- The person can control the composition of the board of directors of a corporation.

- The person is able to cast, or control the casting of, more than 50% of the maximum number of votes that might be cast at a general meeting of a corporation.

- The person holds more than 50% of the issued share capital of a corporation.

The term 'person' includes a corporation. Further, for both (1) and (2) a person or corporation is considered to be able to control the composition of the board of directors of a corporation if that person or corporation can appoint or remove all or a majority of the directors.

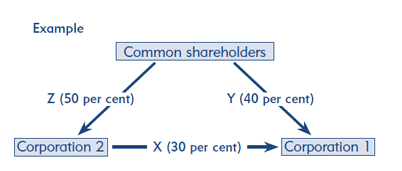

- A corporation, together with its shareholders, holds more than 50% of the issued share capital of another corporation. This will be deemed to have occurred where both of the following conditions are satisfied:

- (a) X + Y > 50%

- (b) X + Z > 50%

where:- X is the shareholding in corporation 1 held by corporation 2 expressed as a percentage.

- Y is the shareholding in corporation 1 held by the shareholders common to both corporations expressed as a percentage.

- Z is the shareholding in corporation 2 held by the shareholders common to both corporations expressed as a percentage.

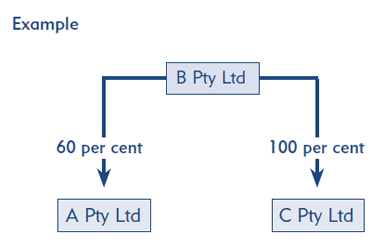

- One corporation is related to another corporation and that second corporation is, in turn, related to a third corporation, the first corporation and the third corporation will also be related. Therefore, all 3 corporations will be taken to be related.

A forms a group with B because B holds more than 50% of the issued capital of A. For the same reason, B forms a group with C. Therefore A, B and C form one group as B is the common member of both groups.

Important points

- Corporations can be grouped even though they do not own land in Victoria.

- The term 'issued share capital' does not include shares which carry no right to participate in a distribution of profits or capital beyond a specified amount (i.e. preference shares).

- A person does not need to have a controlling interest in 2 corporations by the same means for a group to exist (i.e. a person can control the composition of the board of directors of one corporation and hold more than 50% of the issued share capital of another).

- Shares held or power exercisable by a trustee or nominee will be treated for grouping purposes as also being held by the beneficial holder.

- Shares held or power exercisable by virtue of a debenture, or a trust deed for securing the issue of debentures, shall be disregarded.

- Shares held or power exercisable by a person or corporation, whose business includes the lending of money, shall be treated as not held by that person or corporation provided that the shares are held or the power exercisable merely as a security over a transaction entered into in the course of that business.