On 1 July 2025, the Victorian Government announced a short-term extension of the Victorian Homebuyer Fund until allocated funds are exhausted.

Homebuyer Fund

The Victorian Homebuyer Fund supports thousands of Victorians to enter home ownership.

The Victorian Homebuyer Fund is a shared equity scheme, making it easier for Victorians to enter home ownership.

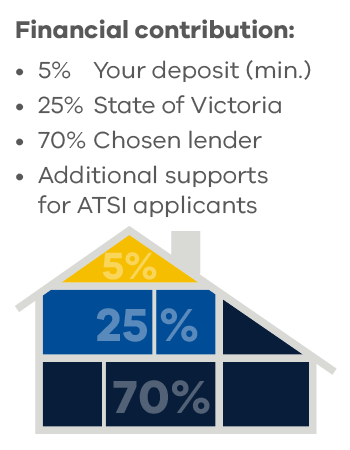

If you have a 5% deposit, the Victorian Government could contribute up to 25% of the purchase price in exchange for an equivalent share in the property. This will save you money by reducing your mortgage and removing the need for Lenders Mortgage Insurance.

Aboriginal and Torres Strait Islander participants only require a 3.5% deposit and are eligible for up to a 35% shared equity contribution.

Participants are required to buy back the government’s share in their property over time through refinancing, using savings, or upon sale of the property. The Victorian Government does not charge interest on its investment in participants’ homes, but shares in any capital gains or losses proportionate to its share in the property.

Want to speak with us about the Victorian Homebuyer Fund? Contact us on (03) 7020 1549 between 8.30 am and 5 pm (AEST), Monday to Friday, excluding public holidays.

Who is eligible for the Victorian Homebuyer Fund?

To be eligible to participate in the Victorian Homebuyer Fund, you need to:

- be an Australian or New Zealand citizen, or permanent Australian resident

- be at least 18 years of age at settlement

- have saved the required minimum deposit (at least 5% or 3.5% for Aboriginal and Torres Strait Islander participants) of your property price

- earn $140,230 or less per annum for individuals (excluding single parents), or $224,370 or less per annum for single parents or joint applicants. This refers to your gross annual income

- occupy the purchased property as your principal place of residence

- be a natural person (that is, not an organisation, company, trust or other body or entity)

- not purchase your property from a vendor who is a related person

- not own an interest in any land in Australia or overseas at the time of purchase (including as trustee of a trust or beneficiary under a trust)

- not be a shareholder in any corporation (other than a public company) that owns any land in Australia or overseas

- have an approved loan from a participating lender and have sufficient funds to pay all acquisition costs associated with the purchase.

You must meet all of these eligibility requirements. Eligible participants must become registered owners of the property they buy.

Property eligibility

Properties involving stratum title (e.g. ownership through company shares) are not eligible for the VHF, including where stratum title only applies to common property. If in doubt, you should check with the SRO before any contracts are signed and/or become unconditional.

Price caps and locations

Participants can purchase an eligible property in any location in Victoria.

The property must be a residential property such as a house, townhouse, unit or apartment (vacant land is not eligible). The maximum purchase price must be $950,000 or less in metropolitan Melbourne and Geelong, or $700,000 or less in regional Victoria.

Maximum purchase prices for locations

The purchase can be for an existing or new property, provided that a certificate of occupancy has been issued prior to the date of the contract of sale. This means off-the-plan property purchases are not eligible.

The property must also be vacant when purchased or, if under a lease, the lease must expire within 12 months of the acquisition date and any tenants must vacate the property.

Your ongoing obligations

If approved for the Victorian Homebuyer Fund, there are a range of ongoing obligations you are required to fulfil.

How to apply

Before applying for the Victorian Homebuyer Fund, you should check your eligibility and read our frequently asked questions.

After checking your eligibility (via our eligibility tool) you should gather the required documentation to apply for a home loan, such as payslips, bank statements and tax returns, and speak to a participating lender.

Apply for the Victorian Homebuyer Fund

The State Revenue Office administers the Victorian Homebuyer Fund. All information provided to participating lenders and referred for the purposes of scheme participation will be managed in accordance with both the State Revenue Office’s privacy policy and the Department of Treasury and Finance’s privacy statement.

First Home Owner Grant, duty exemptions and concessions

In addition to the Victorian Homebuyer Fund, you may also be eligible for a range of other grants, exemptions or concessions. Find out more on our buying a property page.

Last modified: 16 July 2025

News and updates

-

1 July 2025

Short-term extension of Victorian Homebuyer Fund

-

3 December 2024

State Taxation Further Amendment Act 2024

-

20 November 2024

State Revenue Office 2023–24 Annual Review is now available